London has long been a stable location for overseas investors wishing to invest in the UK residential investment property.

Clear legal ownership structures, including freehold and leasehold, a familiar and well-known asset class, and accessible financing options have all contributed to making the UK—particularly London—an attractive destination for overseas investors.

Lower interest rates and advantageous currency movements have contributed to increased investor interest in the UK residential property market.

The Market

The prime London market continues to remain attractive to overseas investors given recent stock market volatility; prime London is still seen as a “safe harbour” and as a longer-term investment.

The change in non-Dom rules (now long-term residents) has led to exits from the capital, but rental returns remain solid with yields in the range of 2.5-3%.

Interest Rates

As fixed rates continue to fall and additional Bank of England rate cuts are expected, transaction activity is on the rise. Financing for Ultra High Net Worth Individuals (UHNWIs) generally ranges between 50% and 60% loan-to-value.

Currency

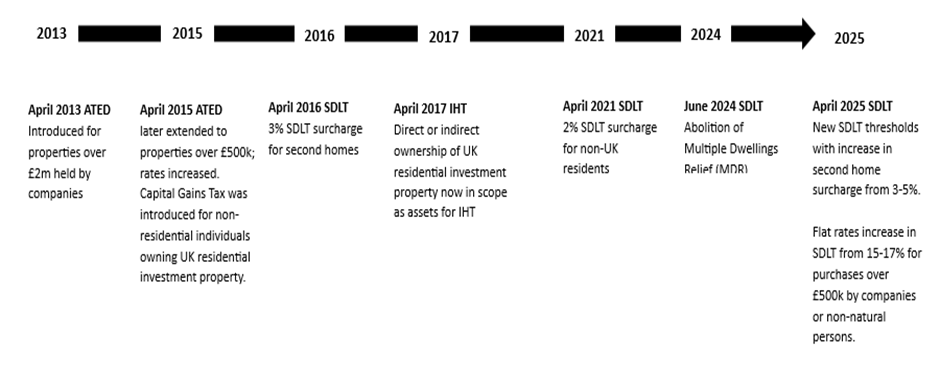

Exchange rate advantages in select jurisdictions relative to the British Pound (GBP) have presented potential discount opportunities for overseas investors. The principal challenge, however, is taxation, which has seen numerous amendments since 2013 under George Osborne and subsequent chancellors.

Despite the changes, investments in new properties or refurbishments to existing properties continue to happen. At Boston Multi Family Office, our overseas UK property investors tend to favour the property market as a longer-term family succession strategy and given the use of finance and general costs of owning a London investment property are less concerned with tax on rental profits (lower yields in central, prime London coupled with interest and general property costs tend to act as a tax mitigant), Capital Gains, (our clients see the investment properties as long-term family succession assets and are less likely to sell, however further tinkering with rates and reliefs have brought CGT into focus) but since 2017 the big concern has been Inheritance Tax “IHT”.

IHT – Inheritance Tax

All directly held UK assets are within the scope of IHT (at 40 per cent), whether the owner is domiciled in the UK or abroad (or, from 6 April 2025, a long-term UK resident or not).

From 6 April 2025, the concept of domicile will no longer apply and will, instead be replaced by whether the individual is a long-term UK resident. An individual who has been UK resident for 10 or more tax years out of 20 will be a long-term UK resident and (subject to tapering provisions) will remain so until he or she has ceased to be UK resident for 10 tax years.

Since April 2017, where the asset in question is UK residential investment property, it will come directly or indirectly within the scope of IHT. If the property is held in an offshore company, the shares in that company come within the scope of IHT.

Professional advice should obtained to ensure that the best strategies and structures are put in place. Below are a few examples.

Personal Ownership

Owning property personally is straightforward and avoids the administrative burden of setting up and maintaining a company or Trust structure and the UBO retains full control over the property asset and all decision making.

On the downside:

- High SDLT, 2% non-resident surcharge and 5% surcharge for additional properties. This can result in up to 19% SDLT on high level purchases.

- Income tax on rental profits at personal rates.

- Personal ownership is publicly recorded at the Land Registry.

- Inheritance Tax (IHT) – UK property owned personally is subject to tax at 40% regardless of where they are resident.

Overseas Company

Historically overseas companies could offer a degree of privacy, although still effective beneficial ownership registers in the relevant jurisdiction will provide UBO details.

There may be tax savings available on acquiring shares such as SDLT savings, but this is often incorporated into the sales price and corporate tax rates are lower regarding tax on rental profits.

The offshore company route can also be beneficial when it comes to transferring property assets between generations at a later stage.

On the downside:

- ATED & SDLT – if not rented commercially, ATED charges and higher SDLT could apply.

- Compliance with the UK Register of Overseas Entities came into force on 1st August 2022.

- IHT – as the underlying asset is a UK residential investment property, the share value (even though offshore) will be subject to IHT at 40%.

Offshore Trust

As with previous Boston Multi Family Office insights, Offshore Trusts offer several advantages when it comes to Family Succession Planning, asset protection from creditors or legal claims in the family’s home jurisdiction. A degree of control is also on offer as to how assets are managed and distributed even after the settlor’s death.

On the downside:

Trust and company structures were popular holding vehicles up to April 2017 but since then UK residential investment property held directly or indirectly by Offshore Trusts is subject to UK IHT. This can include, Trust entry changes, a 10-year anniversary change of up to 6% and exit charges if removing property or shares out of the structure.

The UK Authorities also require compliance with the Trust Registration and Register of Overseas Entities.

Conclusion

General London prime market conditions remain favourable and with further interest rate reductions expected coupled with a potential discount based on currency, the Boston Multi Family Office clients continue to view London prime UK residential investment property as an essential asset for long term family succession planning.

We touched on several structures which could apply and how to mitigate some of the tax risks by utilising an Offshore Family Trust. Other planning includes, to consider life insurance written in Trust to pay a potential future IHT bill and longer-term retirement vehicles linked to specialist Trusts can also be a consideration.

As always, planning and professional advice is required and at Boston Multi Family Office, we can support this with our in-house team in Jersey, the UK, Malta and the Isle of Man. In conjunction with our network of specialists in legal, tax, financing and property matters.

How can Boston Multi Family Office Help?

At Boston we recognise that each family’s circumstances and values are unique. Our experienced team collaborates with you and your advisors to design and implement structures that safeguard your family’s long-term security, foster cohesion, and support enduring success.

We are ideally positioned to assist family businesses that wish to expand internationally. We are a multi-jurisdictional fiduciary service provider with offices in the Isle of Man, Jersey, Malta and the UK that implement tailored governance solutions to clients. Should you wish you to discuss the topic in more detail or interested to hear how Boston Multi Family Office can assist you, please contact enquiries@bostonmfo.com